Application of Digital Financial Services

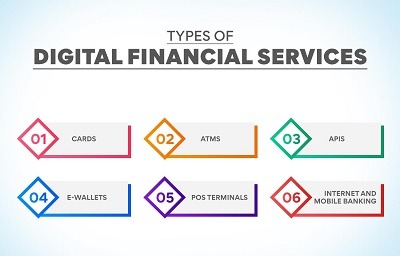

Digital financial services (D F S) encompass a wide range of financial products and services that are delivered through digital channels such as mobile phones, the internet, and other electronic platforms. These services have transformed the financial industry and have a broad range of applications. Here are some of the key applications of digital financial services:

- Mobile Banking: Digital financial services enable people to access their bank accounts, check balances, transfer funds, and perform various banking transactions using mobile devices. This is especially important for people in remote or underserved areas who may not have easy access to physical bank branches.

- Digital Payments: Digital financial services facilitate various forms of digital payments, including peer-to-peer transfers, bill payments, and online shopping. Common methods include mobile wallets, digital payment apps, and online payment gateways. These services offer convenience and security.

- Microfinance: DF S has played a significant role in microfinance by making it easier for microfinance institutions to disburse and collect loans. This has helped individuals and small businesses access credit and manage their finances more efficiently.

- Remittances: Many people working in foreign countries send money back home to their families. Digital financial services offer a more cost-effective and convenient way to send and receive remittances compared to traditional money transfer services.

- Savings and Investments: Digital platforms provide opportunities for individuals to save and invest their money. This includes digital savings accounts, robo-advisors, and investment apps that make it easier for people to grow their wealth.

- Insurance: Digital financial services enable people to access insurance products, pay premiums, and make claims online. This makes insurance more accessible and affordable to a broader population.

- Government Payments: Governments use DFS to disburse social welfare payments, pensions, and subsidies directly to beneficiaries’ bank accounts, reducing leakage and ensuring that funds reach the intended recipients.

- E-commerce Financing: Digital financial services can facilitate financing options for online shoppers, allowing them to make purchases on credit or in installments.

- Cryptocurrencies and Blockchain: While not a traditional DFS, cryptocurrencies and blockchain technology have the potential to disrupt the financial services sector by providing decentralized and secure digital currency and financial infrastructure.

- Digital ID and Authentication: Strong digital authentication and identification methods are a key enabler of digital financial services, allowing users to securely access their accounts and perform transactions online.

- Financial Inclusion: Digital financial services have the potential to bring financial services to people who were previously excluded from the formal banking system, such as those in rural or unde r served areas. It can help reduce the financial inclusion gap.

- Risk Management: Businesses and individuals can use digital financial services to manage various financial risks, including currency risk, market risk, and operational risk through tools like hedging services and derivatives.

- Financial Literacy and Education: DF S providers often offer financial education and literacy resources to help users make informed financial decisions.

The application of digital financial services has the potential to improve financial access, reduce the cost of financial transactions, increase financial literacy, and drive economic growth in many regions. However, it’s important to address issues related to security, privacy, and regulatory frameworks to ensure the responsible and effective use of these services.

The successful application of digital financial services (DF S) requires several key elements and considerations. These requirements are essential for both providers and users to make the most of these services. Here are some of the key requirements for the application of digital financial services:

- Access to Digital Infrastructure:

- Access to internet connectivity and mobile devices is crucial for users to access digital financial services. Infrastructure development is necessary to ensure widespread access, especially in under served or rural areas.

- Digital Literacy:

- Users need to be digitally literate to navigate digital financial services effectively. Educational initiatives and user-friendly interfaces are essential to bridge the digital literacy gap.

- Regulatory Framework:

- A well-defined and supportive regulatory framework is necessary to ensure the legality, security, and consumer protection in digital financial services. Regulations should strike a balance between innovation and protection.

- Security Measures:

- Robust security measures are crucial to protect users’ financial information and transactions. This includes encryption, multi-factor authentication, and fraud detection systems.

- Data Privacy:

- Providers must adhere to data privacy regulations to protect users’ personal and financial data. Privacy policies and user consent should be transparent and respected.

- Interoperability:

- Ensuring that different DF S providers and platforms can work together seamlessly is vital. This allows users to transfer money and access services across various providers without friction.

- Customer Support:

- Efficient and accessible customer support is essential for users to resolve issues and get assistance when using digital financial services.

- Trust and Credibility:

- Trust is paramount in financial services. Digital providers must establish a credible reputation to gain and maintain users’ trust. This includes transparent pricing and effective dispute resolution.

- Financial Inclusion:

- Efforts should be made to include under served and marginalized populations in the digital financial ecosystem. This may involve creating simplified account opening procedures and designing services tailored to their needs.

- Payment Infrastructure:

- Digital payment infrastructure, including mobile wallets, online payment gateways, and digital point-of-sale systems, should be readily available and easy to use.

- Partnerships:

- Collaborations and partnerships between DF S providers, banks, fintech firms, and other stakeholders can expand the range of services and reach a broader user base.

- Affordability:

- Digital financial services should be affordable for users, especially in low-income or remote areas. High transaction costs can deter adoption.

- User-Centered Design:

- Services should be designed with the user’s needs in mind. User-friendly interfaces and simple processes make DFS more accessible and appealing.

- Financial Education:

- Users need access to financial education and literacy programs to make informed decisions about their finances and how to use digital services effectively.

- Scalability:

- Digital financial services should be scal able to handle an increasing number of users and transactions without compromising performance or security.

- Anti-Money Laundering (AM L) and Know Your Customer (KY C) Compliance:

- DF S providers must comply with AM L and KY C regulations to prevent illicit financial activities and ensure the legitimacy of their users.

- Adaptation to Local Contexts:

- DFS offerings should be tailored to the specific needs, preferences, and cultural contexts of the target user base. One size does not fit all.

The successful application of digital financial services is a complex undertaking that involves not only technological infrastructure but also social, regulatory, and economic considerations. Providers, governments, and international organizations often collaborate to create an environment conducive to the responsible and effective use of digital financial services.

The successful application of digital financial services (D FS) involves various stakeholders who play critical roles in enabling and sustaining these services. These stakeholders include:

- Financial Service Providers (FS P s):

- Traditional banks, microfinance institutions, fin tech companies, and payment service providers are essential stakeholders in offering DFS. They develop and maintain the digital platforms and services that users access.

- Regulators and Government Authorities:

- Governments and regulatory bodies are responsible for creating and enforcing the legal and regulatory framework within which digital financial services operate. This includes overseeing consumer protection, data privacy, and financial stability.

- Telecom Operators:

- Telecom companies provide the necessary mobile and internet infrastructure for users to access digital financial services. They often collaborate with FSPs to facilitate mobile banking and mobile money services.

- Users/Clients:

- Individuals and businesses are at the core of digital financial services. They use these services for banking, payments, savings, investments, and more.

- Technology Providers:

- Technology companies and solution providers offer the software, hardware, and technical infrastructure required for digital financial services. They may provide payment gateways, security solutions, and customer relationship management tools.

- Agent Networks:

- In many regions, digital financial services rely on agent networks, which consist of physical locations where users can interact with a human agent to conduct transactions, cash-in/cash-out, and other services.

- International Organizations and Donors:

- Organizations such as the United Nations, the World Bank, and donor agencies often provide support and funding to promote financial inclusion and the development of digital financial ecosystems in under served areas.

- Consumer Protection Organizations:

- Organizations and agencies focused on consumer rights and protection help ensure that users of digital financial services are treated fairly and that their financial rights are upheld.

- Educational Institutions:

- Educational institutions, including universities and vocational training centers, can play a role in educating individuals about digital literacy and the responsible use of DF S.

- Security and Compliance Experts:

- Experts in cyber security and regulatory compliance are crucial to ensuring the security and legality of digital financial services. They help protect against fraud, data breaches, and other security threats.

- Market Infrastructure Providers:

- These organizations support the financial market infrastructure, such as payment clearing and settlement systems, which underpin digital transactions and ensure they are executed smoothly and securely.

- Community Leaders and NGOs:

- Local community leaders and non-governmental organizations can help promote awareness and adoption of digital financial services, particularly in areas where financial inclusion is low.

- Entrepreneurs and Startups:

- Innovators and entrepreneurs often lead the development of new digital financial solutions, from mobile banking apps to peer-to-peer lending platforms.

- Partnerships and Collaborations:

- Collaboration between different stakeholders is often necessary for the success of DF S. Partnerships between FSPs, telecom operators, and other entities can help create integrated and comprehensive DFS ecosystems.

The success of digital financial services depends on the cooperation and coordination of these stakeholders, as well as the development of a supportive ecosystem that combines technology, regulation, and user education to foster financial inclusion and enhance the overall financial landscape.

When is required Application of Digital Financial Services

The application of digital financial services (DF S) is required in various situations and scenarios, as they offer numerous advantages and can address specific needs and challenges. Here are some instances when the application of DFS is necessary or highly beneficial:

- Financial Inclusion: DF S is crucial for providing financial services to individuals and communities that are under served or excluded from the traditional banking system. This can include people in rural areas, low-income populations, and those without easy access to physical bank branches.

- Remote and Under served Areas: In regions with limited infrastructure and banking services, DFS can be a lifeline, allowing people to access banking, payments, and other financial services using digital channels.

- Emergency Aid and Relief: During natural disasters, emergencies, or humanitarian crises, DF S can facilitate the rapid disbursement of funds to affected populations, enabling quick access to financial support.

- Cross-Border Transactions: DF S is beneficial for international remittances and cross-border trade, where it offers a more cost-effective and efficient way to transfer money and make international payments.

- Small and Medium-sized Enterprises (SMEs): SMEs often rely on DF S for their financial needs, including payment processing, credit, and access to financial tools that can help them grow and manage their businesses.

- E-commerce and Online Business: In the digital age, e-commerce businesses rely on digital payment solutions to facilitate online transactions, improving convenience for customers and business owners.

- Government Payments: Governments use DF S to distribute social welfare payments, pensions, and subsidies, reducing leakage and ensuring funds reach the intended recipients. This is especially important for social safety net programs.

- Financial Services Innovation: DF S supports innovation in the financial sector, fostering the development of new financial products, services, and business models that cater to evolving consumer needs.

- Personal Finance Management: Individuals use digital financial services to manage their personal finances, including savings, investments, budgeting, and retirement planning.

- Security and Fraud Prevention: DF S often includes advanced security features and fraud detection mechanisms, making it necessary for secure and reliable financial transactions in the digital age.

- Real-time Transactions: The speed of digital transactions makes them necessary in scenarios where immediate payment confirmation and access to funds are crucial, such as e-commerce and point-of-sale transactions.

- Financial Literacy and Education: The application of DFS is required in situations where there is a need to enhance financial literacy and educate individuals about responsible financial management.

- Cost Reduction and Efficiency: Businesses and organizations use DFS to reduce transaction costs, increase efficiency, and streamline financial processes.

- Regulatory Compliance: DFS is essential to ensure financial institutions and service providers comply with regulatory requirements, such as anti-money laundering (AML) and know your customer (KY C) regulations.

- International Trade and Investment: Businesses engaged in international trade and investment rely on DF S for foreign exchange transactions, trade finance, and investment management.

The application of DF S is versatile and adaptable, and its necessity often depends on the specific financial needs and circumstances of individuals, businesses, and communities. Digital financial services continue to evolve to meet a wide range of financial needs and challenges in an increasingly digital world.

Where is required Application of Digital Financial Services

The application of digital financial services (DF S ) is required and can be beneficial in various geographic locations and settings. Here are some of the key areas where DF S is important:

- Urban Areas: Digital financial services are commonly used in urban centers to facilitate banking, payments, and financial transactions for residents and businesses. They provide convenience, speed, and efficiency in these settings.

- Rural and Remote Areas: DFS is especially important in rural and remote regions where access to traditional banking services may be limited. It helps bridge the financial inclusion gap by allowing people in these areas to access banking, savings, and payments through mobile phones and the internet.

- Developing Countries: Many developing countries have embraced digital financial services to expand financial inclusion, enhance access to credit, and promote economic growth. These services often play a critical role in improving the financial lives of under served populations.

- Emerging Economies: Emerging economies are increasingly adopting DF S to modernize their financial sectors, enhance access to financial services, and promote economic development.

- Financially Under served Communities: DF S is required in communities with limited access to traditional banking services, including indigenous populations, low-income neighborhoods, and marginalized groups.

- Agricultural Areas: Digital financial services are used to facilitate payments to farmers, enable agricultural financing, and improve access to crop insurance and agricultural information.

- Tourism Hubs: In regions with a high influx of tourists, DFS is important for businesses in the tourism and hospitality sector to accept digital payments from visitors.

- E-commerce and Online Marketplaces: E-commerce platforms and online marketplaces are dependent on digital financial services for processing payments and enabling online shopping.

- Disaster and Crisis Response: DF S is crucial in disaster-prone areas, where it enables rapid, secure, and transparent distribution of emergency aid and relief funds during crises.

- Cross-Border Transactions: In regions with cross-border trade and migrant labor forces, digital financial services facilitate international remittances, trade financing, and cross-border transactions.

- Schools and Educational Institutions: Educational institutions use DF S for fee payments, scholarships, and allowances disbursed to students. This simplifies financial transactions for students and staff.

- Government and Public Services: Governments use DFS for disbursing social welfare payments, pensions, and subsidies. Additionally, digital platforms support tax collection and other government services.

- Healthcare Facilities: Healthcare providers often adopt digital financial services to process payments from patients, manage medical records, and handle health insurance claims.

- Tourist Destinations: Popular tourist destinations frequently implement digital financial services to cater to the payment preferences of international tourists, making it easier for them to spend while traveling.

- Environmental Conservation and Aid: Organizations and agencies involved in environmental conservation and humanitarian aid use DF S for transparent and efficient fund management, particularly in remote areas.

- International Business Hubs: Global business hubs and financial centers rely on digital financial services for cross-border transactions, foreign exchange, and international investments.

The application of digital financial services is versatile and adaptable to different geographic contexts and sectors. These services can be tailored to address specific financial needs and challenges in various regions and settings, enhancing financial inclusion and economic development.

How is required Application Of Digital Financial Services

The successful application of digital financial services (DF S) involves several key implementation steps and considerations to ensure that these services are accessible, secure, and beneficial to users. Here’s how the application of DF S is typically carried out:

- Market Assessment: Start by conducting a comprehensive market assessment to understand the specific needs and challenges of the target population or market. Identify the demand for digital financial services and assess the existing infrastructure and competition.

- Regulatory Compliance: Ensure that you are in compliance with the relevant regulations and licensing requirements. Establish a strong understanding of financial regulations, anti-money laundering (AML) laws, and know your customer (KYC) procedures that apply to your specific region or market.

- Technology Infrastructure: Develop or partner with technology providers to build the necessary infrastructure for offering DF S. This includes creating secure digital platforms, mobile apps, and online banking solutions.

- User On boarding: Design user-friendly onboarding processes that are simple and efficient. Enable customers to open accounts and access services easily while adhering to KYC and AML regulations.

- Education and Awareness: Promote financial literacy and educate users about the benefits and responsible use of digital financial services. This can include workshops, online resources, and outreach programs.

- Partnerships: Collaborate with other stakeholders such as banks, telecom operators, and agent networks to expand your reach and provide convenient access points for users.

- Customer Support: Establish responsive and accessible customer support channels to assist users with their queries, issues, and concerns.

- Security Measures: Implement robust security measures, including encryption, multi-factor authentication, and fraud detection, to protect user data and transactions.

- Data Privacy: Adhere to data privacy regulations and ensure the secure handling of customer data. Establish transparent privacy policies and obtain user consent.

- Service Offerings: Design a range of digital financial services tailored to the needs of your target market. This may include mobile banking, peer-to-peer transfers, savings accounts, microloans, and insurance products.

- Agent Networks: If applicable, create or leverage agent networks to provide users with access points for depositing or withdrawing cash and performing other transactions.

- Interoperability: Ensure that your DF S platform is interoperable with other service providers, allowing users to transfer money and access services across different platforms seamlessly.

- User Engagement: Promote user engagement and retention by offering incentives, rewards, and personalized services.

- Monitoring and Compliance: Continuously monitor and audit your operations to ensure compliance with regulations, detect and prevent fraud, and assess the effectiveness of your services.

- Feedback and Improvement: Collect user feedback and use it to improve your services. Be responsive to user needs and concerns, and iterate on your offerings based on their input.

- Scalability: Plan for the scalability of your DF S platform to handle an increasing number of users and transactions.

- Impact Assessment: Evaluate the social and economic impact of your DF S initiatives on the target population, including improved financial inclusion and economic development.

- Marketing and Promotion: Develop marketing strategies to promote your DFS offerings and reach a wider audience.

- Sustainability: Ensure the long-term sustainability of your DFS initiative by managing costs, generating revenue, and achieving financial viability.

- Adaptation: Continuously adapt to changes in technology, user preferences, and market dynamics to stay competitive and relevant.

The successful application of digital financial services requires careful planning, collaboration with key stakeholders, and a user-centric approach. It’s important to create a supportive ecosystem that not only offers access to digital financial services but also promotes financial literacy and inclusion while adhering to regulatory requirements.

Case Study on Application of Digital Financial Services

Certainly! Let’s look at a hypothetical case study to illustrate the application of digital financial services in the context of a developing country.

Title: “Improving Financial Inclusion Through Digital Financial Services in Rural Ghana”

Background: Ghana is a West African country with a predominantly rural population, where many people have limited access to formal banking services. The government of Ghana, in collaboration with a consortium of financial institutions and technology providers, embarked on a project to improve financial inclusion in remote rural areas of the country. The primary objective was to provide essential financial services to under served communities, empower individuals with access to credit, and promote economic growth.

Implementation:

- Infrastructure Development: The project began with the development of mobile and internet infrastructure in rural areas to ensure that people had access to digital channels. Telecom companies extended network coverage, and the government supported the setup of community Wi-Fi hotspots.

- Collaboration with Banks and Fintech Firms: The project partnered with traditional banks and fintech companies to create a digital banking ecosystem. Local banks adapted their services to be accessible through mobile apps, while fintech firms provided innovative solutions like mobile wallets.

- Agent Network Establishment: To facilitate cash-in and cash-out services, an extensive network of local agents was established. These agents helped users convert physical cash into digital balances and vice versa.

- Financial Literacy Campaigns: An educational initiative was launched to increase financial literacy among the rural population. Mobile apps provided interactive modules on savings, budgeting, and responsible borrowing.

- Government Disbursements: The project partnered with government agencies to distribute social welfare payments and agricultural subsidies directly into the digital wallets of beneficiaries. This reduced leakage and ensured efficient fund distribution.

Outcomes:

- Increased Financial Inclusion: The project resulted in a significant increase in the number of individuals with access to formal financial services. Many previously unbanked and underbanked populations now had access to digital banking.

- Economic Growth: The availability of credit and savings options led to increased economic activity in these rural areas. Small businesses flourished, and farmers had access to microloans for agricultural investments.

- Reduction in Cash Handling: The project contributed to a reduction in cash handling, making transactions safer and more convenient. This also had a positive impact on crime rates in the area.

- Cost Reduction: As more people adopted digital financial services, the cost of conducting financial transactions decreased, benefiting both users and service providers.

- Government Efficiency: Government disbursements became more efficient, reducing bureaucracy and corruption. This, in turn, contributed to improved trust in government services.

- Job Creation: The establishment of agent networks and the growth of digital financial services created employment opportunities in these rural communities.

Challenges:

- Digital Literacy: Many users required significant support and training to adapt to digital financial services, especially among older populations.

- Infrastructure Maintenance: The maintenance of digital infrastructure, particularly in remote areas, presented challenges. Frequent power outages and network issues needed to be addressed.

- Regulatory Compliance: Ensuring regulatory compliance and data security was a continuous concern, requiring ongoing monitoring and updates.

Lessons Learned:

- Community Engagement: Involving local communities in the planning and implementation of DF S initiatives is crucial for success.

- Adaptability: DFS initiatives should be flexible and adaptable to the unique needs and constraints of different regions.

- Financial Education: The success of DFS relies heavily on financial literacy initiatives that empower users to make informed financial decisions.

- Collaboration: Collaborative efforts between the government, financial institutions, and technology providers are essential for the widespread adoption of digital financial services.

This case study demonstrates how a concerted effort to implement digital financial services in rural Ghana led to improved financial inclusion, economic growth, and the empowerment of underserved populations. While challenges exist, the positive impact on the community and the economy is a testament to the potential of DFS in transforming financial landscapes in developing countries.

White Paper on Application of Digital Financial Services

Writing a comprehensive white paper on the application of digital financial services (DFS) is a complex and extensive undertaking. Such a white paper typically includes in-depth research, analysis, and insights on the topic. Below is an outline that you can use as a starting point to develop your white paper on the application of DFS:

Title:

- “Empowering Financial Inclusion: The Application of Digital Financial Services”

Abstract:

- A concise summary of the white paper’s key findings and recommendations.

Table of Contents:

1. Executive Summary:

- A high-level overview of the white paper’s contents, highlighting the importance and impact of DF S.

2. Introduction:

- Introduction to the concept of digital financial services, their evolution, and their significance in today’s financial landscape.

3. Digital Financial Services Explained:

- An in-depth explanation of what digital financial services are, including mobile banking, mobile payments, digital wallets, and more.

4. The Need for Digital Financial Services:

- An exploration of the factors and situations that necessitate the application of DFS, such as financial inclusion, remote and under served areas, and economic growth.

5. Advantages and Benefits of DFS:

- A detailed examination of the benefits of DF S, including financial inclusion, cost reduction, and improved efficiency.

6. Challenges and Barriers:

- An analysis of the challenges and barriers faced in implementing DFS, including regulatory issues, digital literacy, and security concerns.

7. Key Stakeholders in DFS:

- An overview of the various stakeholders involved, including financial institutions, technology providers, regulators, and users.

8. Successful Implementation of DFS:

- A section detailing the steps and considerations for the successful implementation of DFS, including infrastructure development, regulation, and user education.

9. Case Studies:

- Real-world examples and case studies showcasing the application of DFS in different regions, industries, and contexts.

10. Regulatory and Security Considerations:

- An examination of the regulatory landscape surrounding DF S, including KYC, AM L, data privacy, and security measures.

11. Digital Financial Services for Financial Inclusion:

- A deeper dive into the role of DF S in promoting financial inclusion and empowering under served populations.

12. Future Trends and Innovations:

- A discussion of emerging trends, such as blockchain technology, cryptocurrencies, and the potential for further innovation in the DF S space.

13. Risks and Challenges:

- An exploration of the risks and challenges associated with DFS, including cyber security threats, data breaches, and potential economic disruptions.

14. Recommendations:

- A set of recommendations for governments, financial institutions, and other stakeholders to maximize the benefits of DFS while mitigating risks.

15. Conclusion:

- A summary of key takeaways and a call to action for further development and adoption of DFS.

16. References:

- Citations and sources used throughout the white paper.

17. Appendices:

- Additional resources, glossary, and supplementary information.

18. About the Author:

- Brief information about the author or organization responsible for the white paper.

Remember that a white paper is typically a longer, detailed document designed to provide comprehensive information and insights on the chosen topic. You may want to collaborate with subject matter experts, conduct thorough research, and ensure that your information is accurate and up-to-date.